Issue #48: The Split Decision

I built two systems. They disagree. One potentially says go long. The other says 29-to-3 bearish. I have to choose.

Issue #48. We’ve come a long way.

This week I’m not burying the lead: the Macro Regime Engine is getting a complete overhaul. Version 2 drops at the end of this month. The 8th Rule has evolved into something I’m calling The Arsenal. And right now, in real time, my old system and my new system are giving me opposite signals on equities.

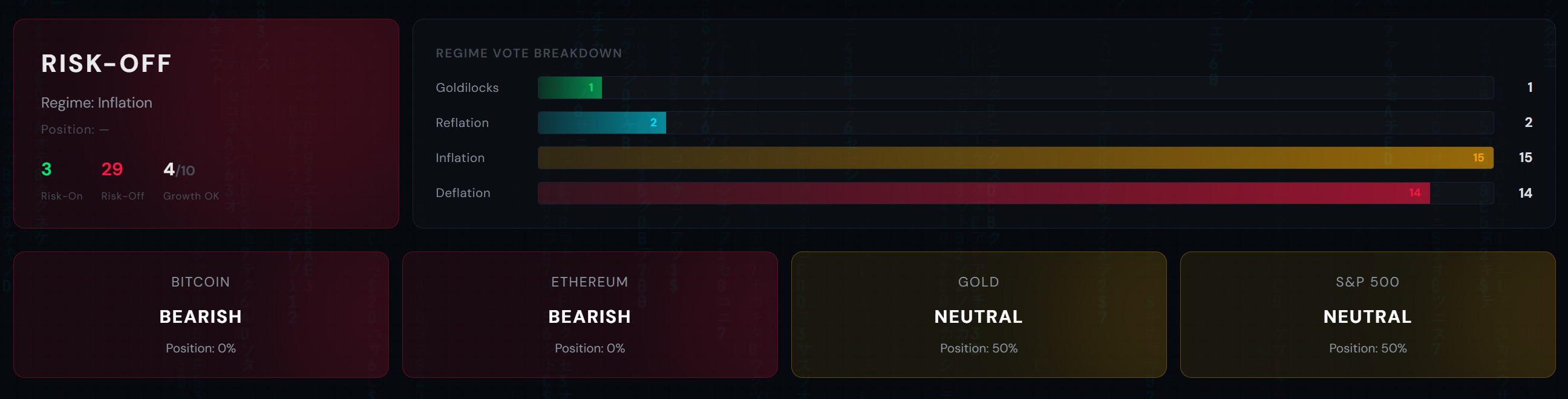

V1 (if things stay the same by Monday open) will potentially flip bullish. V2 is sitting at 29 bearish votes to 3 bullish.

I have to pick a side. And I’m going to walk you through exactly why, with all the numbers, so you can see what I see.

Meanwhile: 25% long Bitcoin, 25% long Ethereum, gold bearish, ~90% still in cash. CPI came in under. The Fed is priced to do nothing for the rest of 2026.

Let’s get into it.

Situation Report: What You Need to Know

MRE V1 (TradingView) might flip bullish for the first time since March 11th. European stocks and Japan turned bullish again. VIX back down. MOVE broke back into bearish. Dollar rolled over. Stress dashboard looking positive.

MRE V2 (Python, standalone) is still overwhelmingly bearish: 29 risk-off votes to 3 bullish as of last night.

The two systems agree 78% of the time. The 22% divergence is almost entirely V2 holding long when V1 has gone flat. Right now is one of those divergence moments.. but in the opposite direction.

Bitcoin: 25% long position initiated this week via The 8th Rule. Signal sent to Substack subs immediately.

Ethereum: 25% long position (discretionary).

Gold: Still bearish. No position.

Portfolio: ~90% cash. Small crypto positions only.

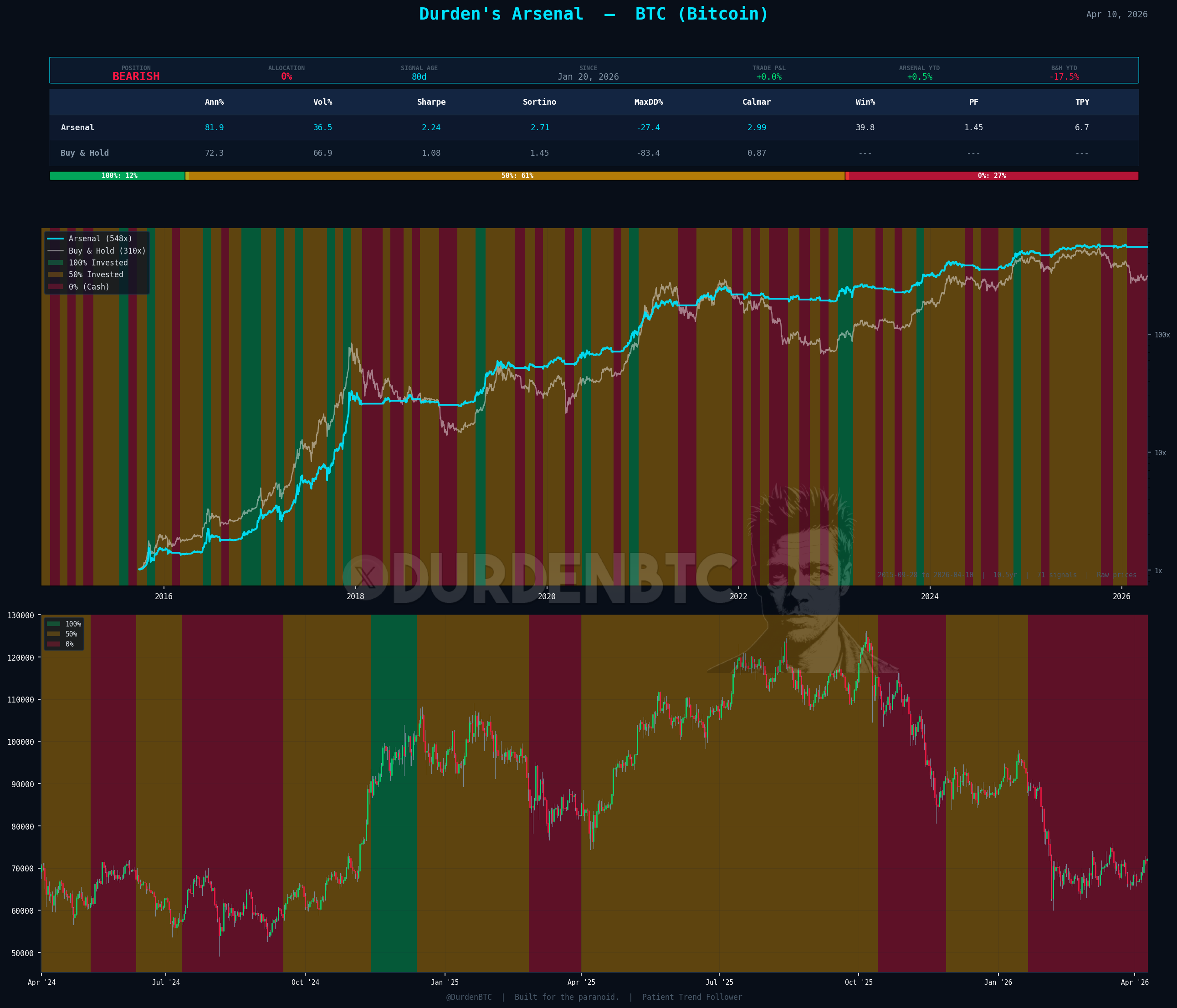

The Arsenal (new indicator replacing The 8th Rule): Sortino of 2.71 on Bitcoin. Beats buy-and-hold (81% vs 72.5% annualized). Max drawdown cut from 94% to 27%. Calmar of ~3. Only fully invested 22% of the time.

MRE V2 performance: 13.4% annual return, Sharpe of 1.06, Sortino of 1.24, max drawdown of 17%. Buy-and-hold: 8.9% annual, 0.47 Sharpe, 56% max drawdown.

The Signal: V1 Says Go. V2 Says Wait.

This is the week where the rubber meets the road on system evolution.

MRE V1.. the TradingView-based engine that’s been running since the Substack launched, has flipped bullish in terms of votes (no trade until potentially Monday open). European stocks turned bullish. Japan turned bullish. Bond volatility (MOVE) broke back down. VIX is back down. Dollar rolled over. The stress dashboard is looking constructive.

But here’s the thing: I’ve spent months rebuilding this entire engine from scratch in Python. Independent of TradingView. And the new version.. MRE V2 as of last night is sitting at 29 bearish votes to 3 bullish.

That’s not a close call. That’s a landslide.

Why rebuild? The issue was never performance.. V1’s backtest is beautiful. The issue was infrastructure. TradingView doesn’t let me export underlying signals day by day. If I want to see how the engine was voting in May 2020, I’d have to manually replay bar by bar. I can’t do proper forward testing. If TradingView changes an asset ticker or goes down, the whole thing breaks. It was brittle. And I needed 1,000% trust in the data, not 95%.

So I rebuilt everything in Python. Standalone. Every signal exportable. Every vote trackable. Full forward testing capability. No dependencies.

And the results are better… by an extreme margin. Enough to make me change the entire infrastructure for what’s running my liquid net worth.

MRE V2 vs V1 vs Buy-and-Hold:

The headline numbers: V2 delivers 13.3% annual return vs 9% for V1 vs 8.86% for buy-and-hold. Sharpe over 1.0 (mic drop). Sortino of 1.2 vs 0.86. Max drawdown is ironically identical at 17%, both systems get clipped slightly differently during the 2008 GFC, but land on the same number.

V1 is notably better at crisis avoidance (completely dodged the 2022 bear and handled COVID beautifully). V2 stays long more often and wins on absolute and risk-adjusted returns as a result.

The key insight from the comparison: V2 wins on returns and risk-adjusted metrics. V1 wins on crisis avoidance. They agree 78% of the time. The 22% divergence is almost entirely V2 holding long when V1 has gone flat.

Right now I’m following V1 for the transition period. By end of month, everything migrates to V2. The rest of April is a side-by-side test.

Bitcoin Trend: 25% Long (But the New System Disagrees)

This is where it gets interesting. The 8th Rule.. the original indicator, fired a long signal earlier this week. Substack subs got the alert immediately. I’m currently in a 25% long Bitcoin position plus a 25% long Ethereum position (discretionary).

But the Arsenal.. the new version of The 8th Rule, disagrees. As of last night, the Arsenal BTC signal is sitting in 100% cash.

Here’s why I built the Arsenal and why the disagreement matters:

The Arsenal uses the same mathematical approach across every asset: three envelopes, purely math-based, OHLC data only, dynamic position sizing. No external correlations. No dependencies. Run it on anything.

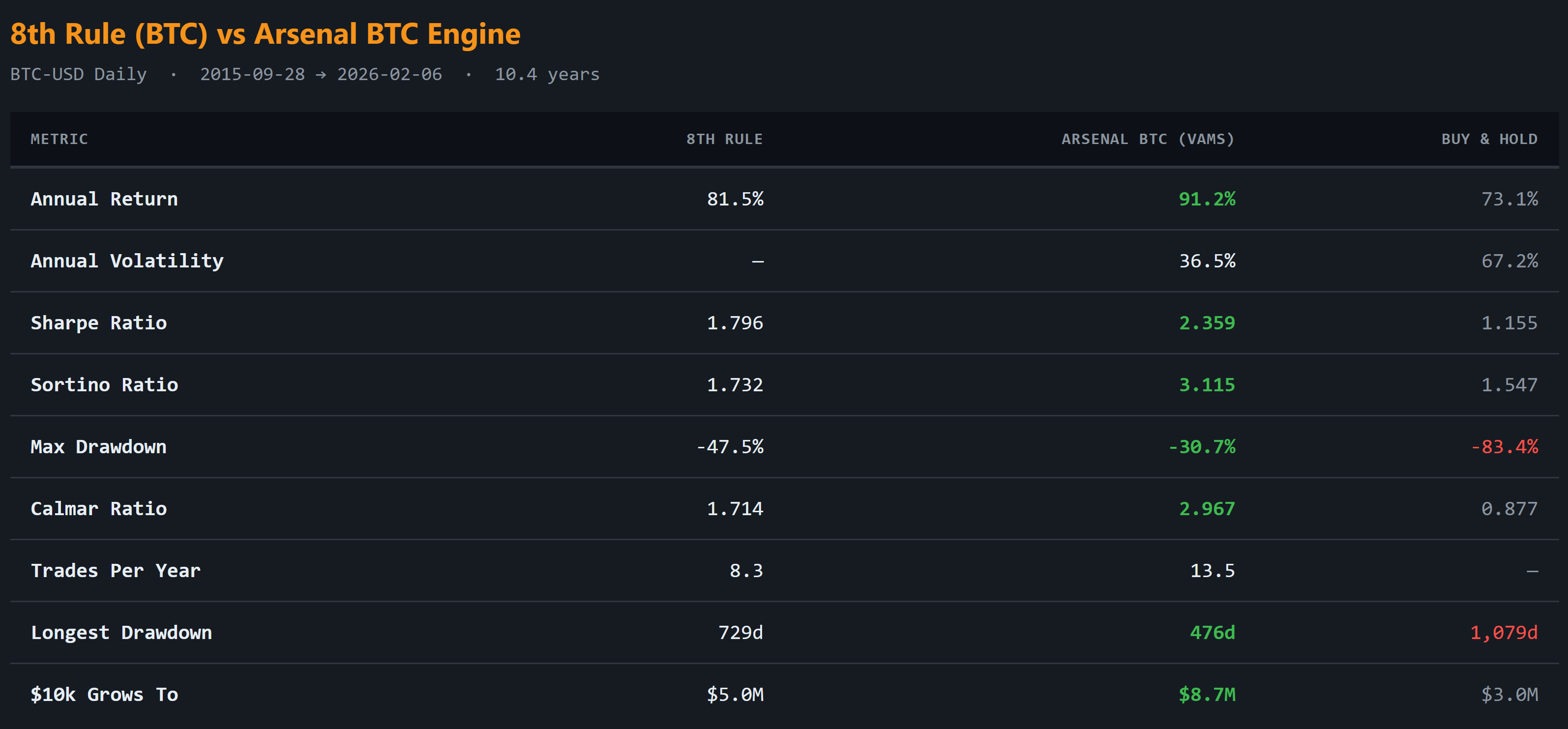

Arsenal BTC vs 8th Rule vs Buy-and-Hold:

Annual return: Arsenal beats both

Sharpe: Huge increase over 8th Rule

Sortino: 2.71 vs ~1.4 — almost double

Max drawdown: 30% vs 47% (8th Rule) vs 94% (buy-and-hold)

Calmar: ~3.0 — almost double the 8th Rule

$10K grows to: $8.7M (Arsenal) vs $5M (8th Rule) vs $3M (buy-and-hold)

The critical insight: the Arsenal is only fully invested (100%) 22.3% of the time. It spends 62% of the time at 50% position size, averaging 63% when invested. It delivers higher returns with dramatically lower drawdowns.. through position modulation, not leverage.

The 8th Rule sits at 100% invested 91% of the time. It captures more upside but takes more pain.

Gold Arsenal: matches buy-and-hold returns but cuts max drawdown from 44% to 13.8%. Calmar of 0.88. Current signal: 50% gold.

SPY Arsenal: Sortino of 1.01, max drawdown of 10.4%. Current signal: 50% position.

All of these: SPY, BTC, Gold, ETH.. will be available in the member dashboard at end of month.

The Data: CPI Drops, GDP Drops, Fed Does Nothing

Quick macro data because this was a systems-heavy letter:

CPI came in under expectations.. inflation dropping, which is good. GDP also dropping, bad for growth, but arguably good because it gives the Fed more room to cut if they need to. The dual decline of inflation and growth is the kind of environment where the Fed has options.

ISM Services missed. Not much else to write home about.

FedWatch: Basically a lock through the end of 2026.. 73% chance rates don’t move at all. Interestingly, December shows a ~20% shot at one cut. So not completely dead, but don’t hold your breath.

TGA dropped slightly.. tax season noise. Nothing structural.

Final Thoughts

The Macro Regime Engine V1 has been excellent. It caught COVID. It dodged the 2022 bear. It went risk-off weeks before this latest selloff. But it’s tied to TradingView, brittle, and impossible to forward test rigorously.

V2 is independent, exportable, testable, and delivers better risk-adjusted returns over 20+ years of data. The Arsenal beats the 8th Rule on every metric that matters.. while being invested less. Position modulation, not leverage. Surgical deployment of capital.

The whole point of these systems is to chop off the left tail.. the brutal, portfolio-destroying crisis drawdowns that leave you homeless. You’ll still have small losses. -2%, maybe -4%. But you keep the entire right side of the distribution. That’s the thesis. That’s the edge.

Right now: V1 says go long. V2 says 29-to-3 bearish. I’m holding small crypto positions (25% BTC, 25% ETH) and sitting in ~90% cash while both systems run side by side through end of month. Then I pivot fully to V2.

48 weekly issues in the books. The systems keep getting better. The edge keeps compounding. And we’re just getting started.

For this weeks full video breakdown:

— Durden out.

✊🧼

Disclaimer: This content is for educational and informational purposes only. It does not constitute financial advice, investment advice, or a recommendation to buy or sell any asset. Trading equities and futures involves substantial risk of loss, including the potential for loss exceeding your initial investment.

Past performance, whether backtested or live, does not guarantee future results. Backtested performance has inherent limitations: it is designed with the benefit of hindsight, does not reflect actual trading, and does not account for all factors that may affect real-world execution.

The author is not a licensed financial advisor. Always do your own research and consult a qualified financial professional before making investment decisions. You are solely responsible for your own trading decisions.